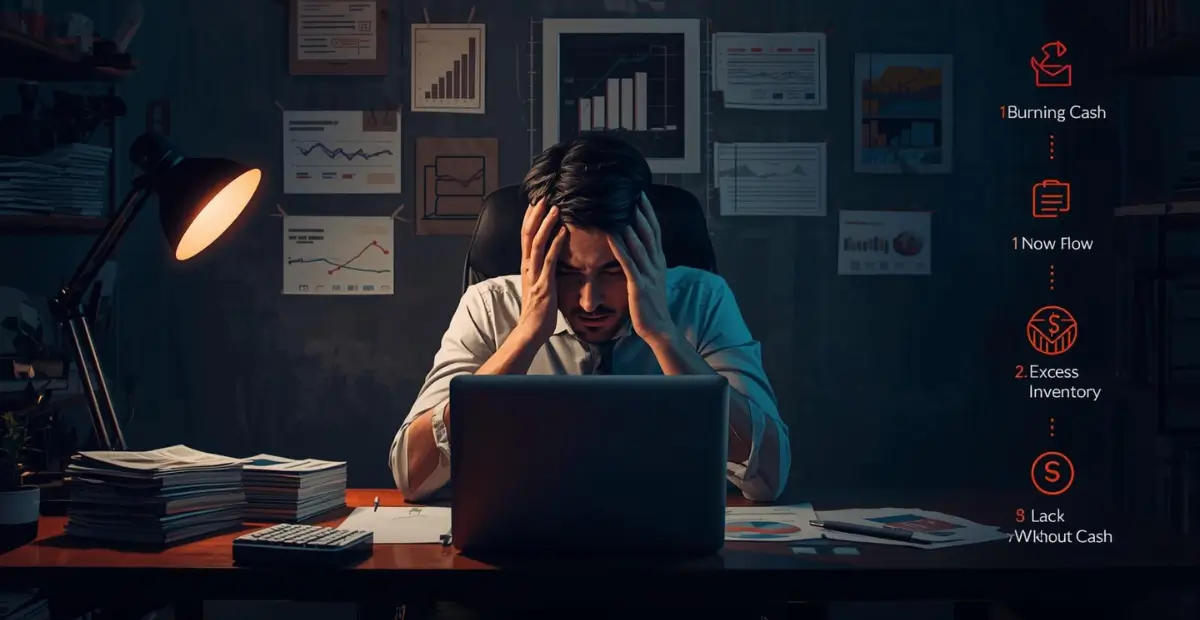

H1: Master Your Money to Survive and Thrive: Avoiding the 5 Fatal Cash Flow Management Mistakes That Sink Startups**H2—1: Opening Insight: The Silent Killer in the Startup World** You have the visionary idea, the passionate team, and a product you believe in. Yet, in the shadows, a silent killer takes down more startups than any failed launch or competitor ever could: poor **cash flow management**. It’s a story as old as entrepreneurship itself. The founder staring at a seemingly healthy bank balance one quarter, only to face a gut-wrenching realization months later that there’s no money to cover payroll. This isn’t just about accounting; it’s about the lifeblood of your venture. Cash flow is the oxygen that fuels every operation, from buying office coffee to securing that critical marketing hire. The emotional toll of mismanaging it—the stress, the sleepless nights, the difficult conversations with employees you care about—is where the human story of business truly unfolds. Understanding **cash flow management** isn’t a financial nicety; it’s the core discipline that separates those who build lasting companies from those who become cautionary tales. **H2—2: Core Concepts Explained Clearly: What Cash Flow Really Means for a Startup** At its simplest, cash flow is the movement of money into and out of your business. Profit is an opinion; cash is a fact. You can be profitable on paper and still go bankrupt if your cash is tied up in unpaid invoices or excess inventory. For a startup, this concept is magnified. You’re burning cash to build, acquire customers, and scale, often long before revenue catches up. This makes precision in **managing your cash flow** not just important, but existential. **H3—2.1: The Three Streams: Operating, Investing, and Financing**Think of your startup’s cash flow as three distinct rivers.* **Operating Cash Flow:** The most critical. This is the cash generated from your core business—payments from customers minus cash paid for expenses like salaries, rent, and suppliers. A positive operating cash flow is the ultimate sign of a healthy, sustainable business model.* **Investing Cash Flow:** Cash used for (or generated from) long-term assets. For a startup, this is almost always negative: buying computers, software licenses, or equipment. It’s cash spent to build capacity.* **Financing Cash Flow:** Cash from investors or lenders (inflows) and cash paid to them as dividends or loan repayments (outflows). This is your runway fuel. **H3—2.2: The Runway Metric: Your Most Important Number**Your **cash runway** is the number of months you can operate before running out of money, assuming no new cash comes in. It’s calculated as: Current Cash Balance / Monthly Burn Rate. If you have $100,000 in the bank and burn $20,000 a month, you have a 5-month runway. This isn’t a static number; it’s the heartbeat you monitor weekly. The goal is to extend it through revenue growth, cost management, or new financing before it gets critically short. **H2—3: Strategies, Frameworks, and Actionable Steps for Proactive Control** Moving from concept to control requires a system. Here is an expert-level framework for proactive **cash flow management**. **Step 1: Implement the 13-Week Rolling Cash Flow Forecast.**This is non-negotiable. Unlike a static annual budget, a rolling 13-week forecast is a living document. You update it weekly, projecting every expected cash inflow and outflow for the next quarter. It forces you to look at the near-term reality: When do big tax payments hit? When is that client payment truly due? This granular view exposes upcoming shortfalls weeks in advance, giving you time to act. **Step 2: Enforce Rigorous Receivables Management.**Your invoicing process is a core business operation.* **Shorten Payment Terms:** Net-30 is standard, but can you offer a small discount for Net-15? Start with Net-15 for new clients.* **Automate & Systematize:** Use accounting software to invoice immediately upon delivery. Set up automatic payment reminders at 7, 3, and 1 day before due, and immediately after a due date is missed.* **Assign Ownership:** Someone on your team must own the receivables ledger, building relationships with client AP departments. **Step 3: Master the Art of Payables Without Damaging Relationships.**While you chase receivables, be strategic with payables.* **Negotiate Terms Upfront:** Before signing with a vendor, negotiate the longest payment terms possible. Can you get Net-45 or Net-60?* **Prioritize Payments:** Use a tiered system. Tier 1 (Critical): Payroll, taxes, essential services. Tier 2 (Important): Key vendors. Tier 3 (Discretionary): Non-essential subscriptions, services. **Step 4: Build a Cash Buffer and Define Triggers.**Aim to maintain a cash buffer equal to at least 1-2 months of operating expenses. More importantly, define pre-set financial triggers. For example: *"If our runway drops below 6 months, we immediately implement a hiring freeze and cut all discretionary spending."* This removes emotional decision-making during a crisis. **H2—4: The 5 Fatal Cash Flow Mistakes and Their Antidotes** **Mistake 1: Confusing Revenue with Cash Inflow**You close a $60,000 annual contract! Celebration is warranted, but depositing the cash is not. If the client pays monthly, you’ve gained $5,000 in cash now, not $60,000. Spending based on the booked revenue will crater your cash position.* **Antidote:** Live by your cash flow forecast, not your P&L statement. Decouple your spending decisions from signed contracts and tie them strictly to actual cash receipts. **Mistake 2: Growing Without a Cash-Aware Model**You achieve product-market fit and customers flood in. Success! But each new customer requires upfront cost in support, server capacity, or hardware. If your unit economics are negative (Cost to Serve > Lifetime Value), you are buying growth, and each new customer accelerates your burn.* **Antidote:** Know your Unit Economics cold. Before scaling, ensure you have a clear, cash-positive path to profitability per customer. Fund growth from gross margins, not just investor capital. **Mistake 3: Poor Timing: The Collections & Payments Mismatch**You pay your suppliers in 15 days but allow your customers 60 days to pay. This creates a cash conversion cycle gap of 45 days where you are financing your customers' purchases. It’s a direct, interest-free loan to them that starves your operations.* **Antidote:** Synchronize your cycles. Negotiate to align payment outflows with inflows. If you must pay a supplier in Net-30, your standard terms should be Net-30 or less. Use milestone payments for large projects. **Mistake 4: Over-Investing in Inventory or Fixed Assets**A retailer stocks up for a forecasted holiday rush that doesn’t materialize. A SaaS company commits to a lavish 5-year office lease. Cash—your most flexible asset—is now trapped in illiquid forms. This limits your ability to pivot or seize new opportunities.* **Antidote:** Embrace lean principles. Use just-in-time inventory systems where possible. Opt for month-to-month or short-term leases, even at a slight premium, to preserve optionality. Rent or finance equipment instead of buying outright. **Mistake 5: Flying Blind: No Real-Time Financial Visibility**“I check our bank balance every Friday” is not financial visibility. A single balance tells you nothing about future obligations. You’re reacting, not planning.* **Antidote:** Implement a cloud-based accounting dashboard (like QuickBooks Online, Xero) that connects to your bank feeds. Review your 13-week forecast vs. actuals weekly with your leadership team. Make data-driven decisions, not guesses. **H2—5: Case Studies: Lessons from the Trenches** **Case Study 1: The Scale-Up That Overheated**A B2B software startup, “TechScale,” raised a Series A round. Fueled by capital, they hired aggressively across all departments and moved into a premium office space, locking in high fixed costs. Their growth was strong, but their cash burn was astronomical. They failed to model how long it would take for new sales hires to become productive and generate cash. By the time they realized their runway had shrunk to 4 months, the market had turned, and raising a new round was impossible. They were forced into drastic, demoralizing layoffs and a distressed down-round.* **The Lesson:** Funding is not revenue. Scale your burn in line with validated, cash-producing growth, not hope. Keep fixed costs variable for as long as possible.**Case Study 2: The Consultancy That Won Too Much Work**“CreativeSolve,” a boutique marketing consultancy, was brilliantly run by its founder, a master salesperson. They landed several large, multi-month projects. Financially, they were “profitable.” But their contracts had 60-day payment terms, and they paid their freelance talent every two weeks. The more projects they won, the more cash they needed to cover the payroll gap. They were literally going broke from success. The founder had to take out a high-interest personal loan to meet payroll, creating immense personal stress.* **The Lesson:** Understand your cash conversion cycle intimately. CreativeSolve’s antidote was to switch to requiring 50% upfront for new projects and renegotiating all contracts to Net-15, which their clients accepted due to their stellar work.**H2—6: Advanced Insights: The Future of Startup Cash Flow Management**The tools and landscape are evolving. Smart founders will leverage technology not just for tracking, but for predictive analysis. AI-powered cash flow tools will move beyond historical reporting to scenario modeling: *“What happens to our runway if customer churn increases by 2%?”* or *“If we delay this hire by 3 months, how does it extend our bridge to profitability?”*Furthermore, the rise of embedded finance will blur the lines. Banking-as-a-Service APIs will allow startups to offer dynamic payment terms, access instant revenue-based financing directly from their invoices, and automate cash allocation—all within their own platforms. The future belongs to founders who treat cash flow data as a strategic asset for decision-making, not a backward-looking report. Preparing for this means building a finance stack that is API-connected and data-fluent from day one, even if you start with simple tools.**H2—7: Final Takeaway: Building a Culture of Cash Awareness**Ultimately, elite **cash flow management** is not the sole responsibility of your CFO or part-time bookkeeper. It’s a company-wide mindset that must be led from the top. When a founder openly discusses runway, celebrates extending the cash conversion cycle by two days, and rewards employees for collecting receivables, it builds a culture of stewardship. Your startup’s resilience is measured not by its valuation during a funding boom, but by the precision with which it navigates the cash cycle through every season. Make cash king, not just in your spreadsheets, but in your daily conversations and strategic choices. That is the discipline that turns a startup with potential into an enduring company.

Cash Flow Management: 5 Fatal Mistakes That Ruin Startups, and How to Avoid Them

{kind=link}